Vauld, a Singapore-headquartered crypto lending and exchange startup, has suspended withdrawals, trading and deposits on its eponymous platform with immediate effect as it navigates “financial challenges,” it said Monday.

The three-year-old startup — which counts Peter Thiel-backed Valar Ventures, Coinbase Ventures and Pantera Capital among its backers and has raised about $27 million — said it is facing financial challenges amid the market downturn, which it said has prompted customer withdrawals of about $198 million since June 12.

Vauld founder and chief executive Darshan Bathija said the startup is exploring restructuring options and has engaged with Kroll for financial advice and Cyril Amarchand Mangaldas and Rajah & Tann for legal advice in India and Singapore.

The startup intends to apply to the Singapore courts for a moratorium. “We are confident that, with the advice of our financial and legal advisors, we will be able to reach a solution that will best protect the interests of Vauld’s customers and stakeholders,” he wrote in a blog post, adding that the startup will make “specific arrangements” for certain customers who need to meet their margin calls.

It’s unclear how many users Vauld serves.

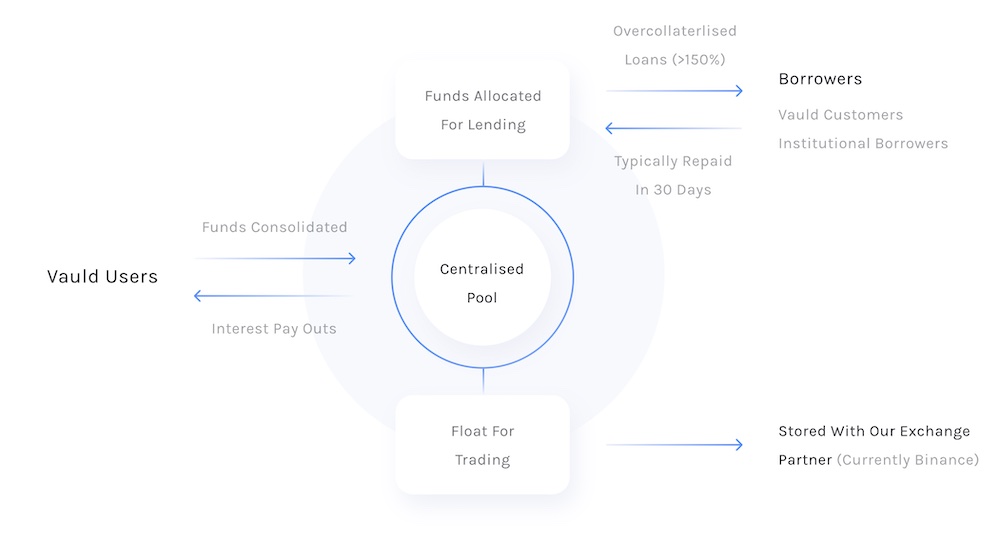

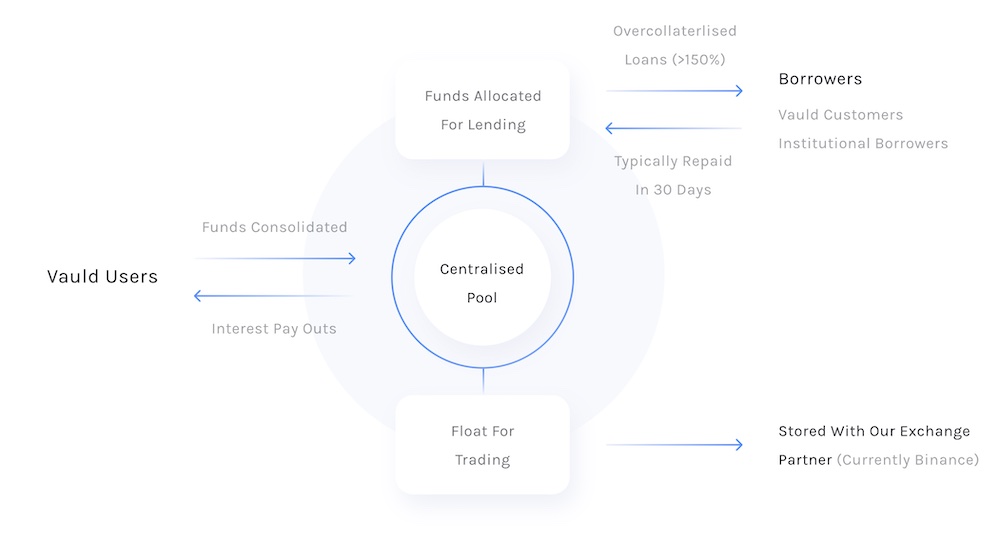

An illustration of how Vauld’s platform worked. (Image: Vauld)

Vauld enables customers to earn what it claims to be the “industry’s highest interest rates on major cryptocurrencies.” On its website, it says it offers 12.68% annual yields on staking several so-called stablecoins including USDC and BUSD and 6.7% on Bitcoin and Ethereum tokens. The platform allowed customers to borrow against their tokens and also facilitated several other trading services.

On its website, Vauld says it offers users the ability to borrow up to an LTV (loan to value) of 66.67% against their tokens and “instantly” approves their loans. Like several tech stocks, many crypto tokens have tumbled by over 70% in value in the past six months.

“We seek the understanding of customers of the Vauld platform that we will not be in a position to process any new or further requests or instructions in this regard. Specific arrangements will be made for customer deposits as may be necessary for certain customers to meet margin calls in connection with collateralised loans,” Bathija wrote today.

The announcement follows Vauld cutting its workforce by 30% two weeks ago.

The move comes as a surprise. On June 16, Bathija assured Vauld customers that the platform had no exposure to Celsius, another lending startup that is facing increasing financial challenges, and Three Arrows Capital, one of the high-profile crypto hedge funds that filed for a Chapter 15 bankruptcy over the weekend.

“We remain liquid despite market conditions. Over the last few days, all withdrawals were processed as usual and this will continue to be the case in the future,” Bathija wrote earlier.

Several crypto veterans including Binance founder and chief executive Changpeng Zhao have warned in recent weeks that many more DeFi platforms are on the verge of facing a collapse. In a recent podcast, Zhao said Binance has engaged with over 50 firms in recent weeks to evaluate funding / bailing out opportunities in some businesses.

“The same deals that you see in the news of other people looking at, they typically come to us first,” he said. “We have the largest cash reserves of any exchange. We like to save the industry as much as possible, but not all projects are worth saving.”

On Friday, FTX’s U.S.-based arm inked a deal with troubled crypto lender BlockFi that gives the crypto exchange the option to buy the startup for up to $240 million based on the startup’s performance. BlockFi, which was among the firms that liquidated at least some positions held by Three Arrows Capital, was valued at $3 billion in a financing round it disclosed in March 2021.